Accurate financial management is essential for any property management business, but for vacation rental managers juggling multiple properties, balancing the books can be particularly challenging. Between early deposits, last-minute cancellations, and overlapping expenses across several platforms, it is easy for details to slip through the cracks. Over time, seemingly small oversights can accumulate into considerable losses, late fees, or even legal complications. The good news is that the most common accounting errors are completely preventable with the right knowledge and systems in place.

Below are five mistakes that vacation rental property managers often encounter. In each case, the reasons these errors occur, their impact on long-term profitability, and the practical solutions to correct them are all outlined. By recognizing these pitfalls and putting measures in place to address them, property management teams can protect revenue and ensure that day-to-day operations run more smoothly.

1. Mixing Personal and Business Funds

One of the most frequent issues in property management is the blending of personal and professional finances. Sometimes, a property manager or team member might be pressed for time and use a personal card to cover supplies, or they might deposit rental income into a personal checking account. While such actions may appear harmless, this practice quickly blurs the lines between personal and business expenses. When tax season arrives or stakeholders request clear financial data, managers often struggle to distinguish legitimate deductions and accurately measure each property’s performance.

From an accounting perspective, mixing funds can trigger audits, complicate month-end closings, and lead to both under- and overestimations of taxable income. Additionally, these unclear financial records compromise the ability to assess which properties are truly profitable. If expenses and revenue aren’t linked to the correct business accounts, a property manager may not recognize which rentals require financial adjustments or operational changes.

A straightforward remedy involves establishing a dedicated bank account (and potentially a separate credit card) exclusively for business use. This approach centralizes all rental income and operational spending, ensuring a more organized bookkeeping process. For teams that include multiple employees or outsourced help, having clear protocols for authorized spending helps maintain consistency. Many property management platforms offer automated expense categorization features, flagging any unusual transactions for review. By cleanly separating personal and business finances, property managers can safeguard against tax complications, streamline internal processes, and gain a clearer perspective of each property’s financial performance.

Handling the Transition from Mixed to Separate Accounts

For those who have already blended personal and business funds, the prospect of untangling past transactions may seem daunting. However, the transition can be managed systematically by:

- Reviewing Past Statements: Collect at least several months’ worth of bank and credit card statements. Determine which transactions were business-related versus personal.

- Consulting an Accountant: A financial professional can help reclassify historical entries, minimizing potential tax or audit issues and ensuring accurate records going forward.

- Closing Out Old Accounts: If a personal account was previously used for property transactions, switch recurring charges and direct deposit settings to the new business account to avoid future mixing.

Taking these steps helps property managers start fresh with accurate data. While it involves some upfront work, the long-term gain of clearer financial boundaries and reduced accounting headaches is well worth the effort.

Connecting Business Accounts Directly to Accounting Software

Once dedicated business accounts are established, linking them to property management or accounting software adds a layer of automation. This integration allows transactions to flow seamlessly into a central dashboard, reducing the need for manual data entry and greatly minimizing human error. Many modern platforms provide real-time categorization for incoming and outgoing funds. By automatically classifying recurring expenses—like cleaning fees, maintenance work, or platform booking fees—software helps maintain consistent records. If an unfamiliar transaction appears, managers are alerted to investigate, further reducing the risk of unaccounted spending.

Training Team Members on Using Company Cards

Even the best systems can fail if staff members are unaware of proper protocols. Team training ensures that everyone involved in the process understands how to use company cards and under what circumstances they should be used. Key training points include:

- Cardholder Responsibilities: Clarify what types of purchases are permitted and which are not, reinforcing that the company card is for business expenses only.

- Receipt Documentation: Encourage employees to log receipts or upload them in real time to the accounting platform.

- Spending Limits: Define clear thresholds for spending, ensuring major costs receive management approval before being charged.

Empowering team members with guidelines on how to handle company accounts keeps finances consistent and transparent. When every participant in the process knows the rules—and the potential consequences of mixing personal and professional transactions—it strengthens overall financial discipline and accuracy.

Practical Implementation

- Open a Dedicated Business Bank Account: Restrict all rental deposits and payments to this account.

- Use a Business Credit Card for Property Purchases: Eliminate confusion by assigning a single card (or set of cards) for legitimate business expenses.

- Integrate with Accounting Software: Streamline record-keeping and monitor transactions through a platform that flags irregularities or missing receipts.

- Train Your Team: Provide clear guidelines on using the company card, enforcing accountability with routine internal audits.

2. Not Keeping Detailed Records and Receipts

In a busy property management operation, thorough record-keeping can easily fall by the wayside. Teams may focus on booking properties, resolving guest concerns, and coordinating repairs—only to let receipts collect in drawers or forget to log smaller transactions. Although these overlooked details might not seem critical at first, they tend to accumulate over time, leading to inaccurate financial statements and missed deductions, especially during tax season.

Without comprehensive documentation, managers risk paying vendors twice for the same service, omitting expenses that should be claimed, or underreporting income from guests. These gaps in record-keeping can also raise concerns during an audit or financial review, where reliable proof of transactions is a necessity.

A strong defense against these pitfalls is implementing a structured, consistent routine for capturing and storing financial data. Using digital tools that allow for receipt scanning, automatic transaction matching, and real-time expense tracking can significantly lighten the administrative burden. Many such systems integrate directly with property management software, extracting transaction details and linking them to individual stays or properties. Scheduling weekly or monthly reviews of all incoming and outgoing funds ensures any anomalies or missing documents are spotted and corrected before they turn into major issues.

Digital Receipt Management Best Practices

- Centralize Your Documentation: Store all receipts—physical and digital—in one central system. Avoid scattering paperwork across email inboxes, filing cabinets, or personal mobile devices. A unified platform saves time and reduces the risk of losing or duplicating records.

- Adopt Mobile Scanning Tools: Modern platforms allow you to snap a quick photo of a paper receipt, then categorize the relevant information (date, vendor, amount). This eliminates the need to track down the paper copy later and ensures details are captured accurately on the spot.

- Set Clear Naming and Tagging Conventions: Establish a standardized method for labeling expenses by property, stay, or department. This makes it easier to search for specific records later and ensures consistent reporting across the business.

- Back-Up Regularly: While most digital tools include cloud storage, maintaining an additional back-up (e.g., on a secure external drive) is a good safeguard against data loss or accidental deletion.

Common Small Expenses That Often Go Undocumented

- Cleaning Supplies and Minor Maintenance Items: Sponges, detergents, light bulbs, filters, and other everyday essentials can add up quickly.

- Travel and Mileage: Reimbursements for staff travel between properties or routine errands sometimes never make it onto the books.

- Petty Cash Purchases: Snacks for open houses, small décor items, or last-minute guest amenities might be overlooked if paid in cash.

- Parking and Tolls: These minor charges, especially for on-site staff or contractors, can slip through the cracks without immediate documentation.

Tracking these small but frequent expenditures ensures you’re not missing out on legitimate deductions or understating your property management costs.

How Modern Mobile Receipt Capture Works

- Receipt Scanning Most modern platforms use your phone’s camera to capture a clear image.

- Cloud Storage and Integration: After scanning, receipts are stored securely in the cloud, accessible from any device with an internet connection. Many apps integrate directly with accounting or property management platforms, enabling seamless updates to financial statements.

- Prompt Notifications: When receipts are processed, both managers and relevant staff receive alerts. This allows for immediate review, error-catching, or reconciliation without waiting until month-end or quarter-end.

By leveraging these tools and best practices, property managers can streamline their financial operations, reduce audit risks, and ensure that every legitimate expense is captured and accounted for.

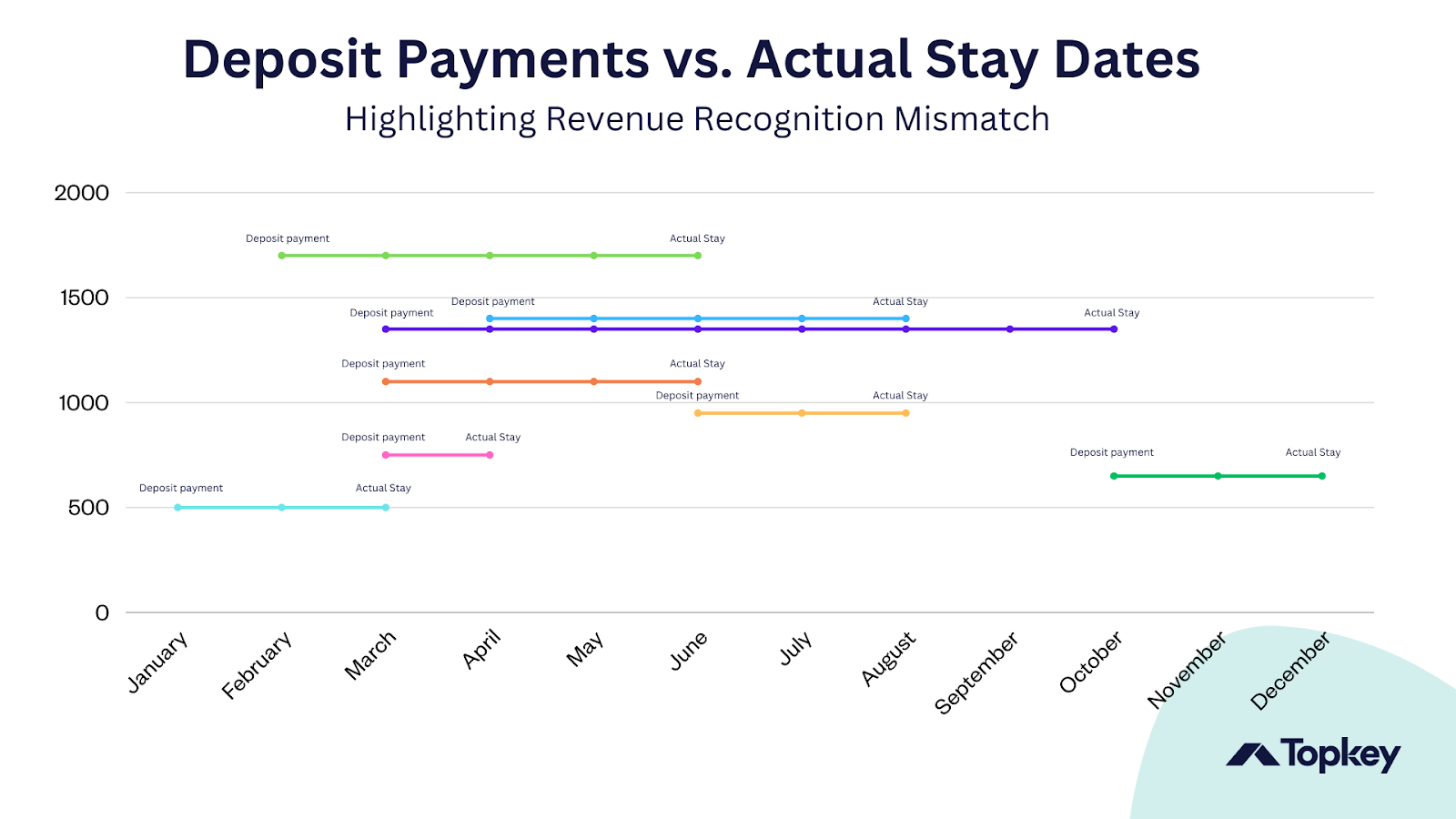

Revenue recognition is another critical element of any accounting strategy, and it can become particularly complex in the vacation rental industry. Deposits might be collected months in advance, final balances might arrive a few weeks before check-in, and refunds or partial payments may arise from cancellations. When teams record all funds as income the moment they arrive, they risk distorting financial statements, making certain months look stronger (or weaker) than they actually are.

This challenge can lead to faulty conclusions about budgeting or future bookings because the reported cash flow may not align with the period when the revenue is actually earned. Managers operating on a purely cash-based system may underestimate or overestimate how profitable a property is at any given time, particularly if payments cross monthly or quarterly boundaries.

A recommended solution is to adopt accrual-based accounting. This approach recognizes revenue in the period it is actually earned, rather than the moment money is received. By aligning guest payments with the time of the stay, managers gain a clearer perspective on monthly or quarterly earnings and can plan accordingly. Many modern vacation rental accounting tools handle staggered payments automatically, tracking deposits and final balances so that the team does not have to manage multiple spreadsheets or manually adjust entries. This prevents major discrepancies and helps property managers make well-informed decisions about pricing, staffing, and reinvestment.

Cash Basis vs. Accrual Basis Accounting

Cash Basis Accounting

- Definition: Under the cash basis, revenue is recorded when you receive money, and expenses are recorded when you pay out money.

- Simplicity: This method is straightforward—money in, money out—and typically requires less complex tracking.

- Potential Pitfalls:

- Revenue spikes or dips may appear in the wrong period if deposits or final payments fall outside of the stay dates.

- It can distort financial health because revenue and expenses are not matched to the periods in which they occur.

- Large advance deposits can make a future month look profitable prematurely. Conversely, expenses paid early might cause an underestimation of profitability during the actual rental period.

Accrual Basis Accounting

- Definition: With the accrual basis, revenue is recognized when it is earned (e.g., when a guest actually stays at the property), and expenses are recorded when they are incurred, regardless of when cash is received or paid.

- Accuracy: This method offers a more accurate view of financial performance because it aligns income and expenses with the actual periods they relate to.

- Complexity:

- Accrual-based accounting can be more involved, often requiring specialized software or deeper accounting knowledge.

- Managing deposits, refunds, and partial payments requires setting up deferred revenue accounts and adjusting entries based on the guest stay dates.

Why Accrual Accounting Matters in Vacation Rentals

- Improved Financial Clarity: By matching revenue to the actual booking period, managers can see true monthly or quarterly profitability. This clarity helps in making better decisions on pricing, staffing, and resource allocation.

- More Accurate Forecasting: Knowing when your revenue is truly “earned” helps forecast future cash flow and budgeting with greater precision. This is vital for property managers juggling multiple properties with varying booking schedules.

- Regulatory and Compliance Benefits: Auditors and financial reviewers often expect accrual-based records because they provide a more reliable snapshot of a business’s financial health. Some jurisdictions may also require accrual accounting once a business exceeds certain revenue thresholds.

- Reduced Risk of Misinterpretation: Large pre-booking deposits or late cancellations can skew financial statements under the cash basis. Accrual accounting ensures these events are reflected in the appropriate time period, minimizing confusion about actual performance.

Implementation Tips

- Adopt Accrual-Based Principles: Educate your team on recognizing revenue when it’s earned and expenses when they are incurred. This shift may require changes to internal workflows and training.

- Utilize Accounting Software with Deferred Revenue Recognition: Choose software or platforms that make it easy to track deposits separately until the stay occurs. Automating this process reduces the chance of human error.

- Maintain Accurate Bookings and Payment Schedules: A robust property management system (PMS) should integrate with your accounting tools to track reservation dates, deposit amounts, and final payment timelines. Keeping these records up to date prevents mismatches and confusion at month-end or year-end.

4. Infrequent Reconciliation

Consistent account reconciliation—cross-referencing internal records with external statements from banks, credit card providers, and booking platforms—is a cornerstone of accurate bookkeeping. However, property management teams often deprioritize this task because immediate day-to-day obligations appear more pressing. When reconciliations are postponed, inconsistencies can go unnoticed for months, creating confusion and complicating the accounting process.

Unresolved discrepancies, such as duplicated charges, missed vendor payments, or unrecorded guest receipts, can be costly. Managers may inadvertently lose revenue by failing to bill the correct amount or overlook additional fees that should have been collected. When these errors surface later, untangling them requires considerable time and effort, complicating month-end or year-end closing.

A best practice is to reconcile accounts on a consistent, predictable schedule—monthly or even weekly. By comparing booking platform payouts, credit card transactions, and bank statements against internal ledgers, teams can promptly resolve mismatches. Many cloud-based accounting solutions pull external transaction data automatically, reducing the reliance on manual entry and highlighting any variances in near-real time. Assigning this as a formal task to an in-house accountant or bookkeeper also helps keep the process consistent. Regular reconciliations foster greater confidence in the numbers used for financial analysis and strategic planning.

Examples of Reconciliation Workflows

- Monthly Bank Reconciliation

- Gather Statements: At the end of each month, download bank statements and credit card statements.

- Compare Transactions: Match each transaction to entries in your accounting software or ledger. Look for missing or additional entries.

- Investigate Variances: If you notice amounts that do not match—e.g., a deposit for $1500 in your bank statement but $1350 in your ledger—verify the correct amount by cross-checking booking receipts or vendor invoices.

- Finalize and Document: Mark any corrected items, add explanatory notes, and ensure your adjustments are reflected in both your accounting software and bank balances.

- Weekly Booking Platform Payout Check

- Identify Scheduled Payouts: Review upcoming payouts from platforms like Airbnb or Vrbo.

- Cross-Reference Internal Records: Confirm that each incoming payment aligns with the correct reservation and that the amounts match what you’re expecting after fees.

- Adjust if Needed: If a platform fee changes or a refund is issued, log the adjustment in your accounting system so the final amount matches the bank deposit.

- Notify the Team: If you spot repeated underpayments or missing payouts, notify relevant stakeholders or the platform’s support team to resolve the issue promptly.

- Vendor and Contractor Payment Reconciliation

- Collect Vendor Invoices: Maintain a central repository of all vendor and contractor invoices related to cleanings, repairs, or maintenance services.

- Match Payments: Verify that each invoice has a corresponding payment in your bank or credit card statements.

- Update Payment Status: If an invoice remains unpaid or partially paid, rectify the situation—either by issuing payment or by correcting your records if the invoice was already settled.

- Follow-up: If vendors claim they have not been paid but your records show otherwise (or vice versa), investigate with both parties to find and fix the discrepancy.

What to Look for During Reconciliation

- Missing Transactions

- Guest Payments: Have all guest payments been properly recorded—especially if they were split into deposits and final balances?

- Refunds: Are all cancellations or partial refunds accounted for, and do they match your bank or booking platform statements?

- Vendor Fees: Sometimes, ongoing or subscription-style services might go unlogged, creating unrecognized expenses.

- Duplicated or Erroneous Entries

- Multiple Charges: Watch out for any duplicated charges or inadvertent double-entry of payments.

- Wrong Amounts: Even minor discrepancies add up over time. A small typo could mean your monthly totals are off by a noticeable margin.

- Timing Differences

- Cross-Period Entries: Payments that arrive at the end of one month and clear in the next can create confusion. Make sure you correctly classify them in the right period.

- Pending Transactions: Credit card payments or platform payouts can take a few days to finalize. Ensure that your reconciliation accounts for this delay.

- Unusual or One-Off Items

- Chargebacks: If a guest disputes a charge, confirm whether your statements show a reversed payment.

- Manual Adjustments: Any manual credits or debits should be clearly documented and explained.

- Non-Recurring Fees: Special maintenance projects or insurance claims can pop up unexpectedly—make sure they’re captured accurately.

- System or Platform Errors

- Booking Platform Miscalculations: Sometimes, platform fees or taxes are misapplied. Double-check the amounts you receive align with expected commissions or local tax rates.

- Software Integration Glitches: If you rely on automated import tools, occasionally review to ensure your system isn’t skipping or duplicating transactions.

Benefits of Frequent Reconciliation

- Early Error Detection: The more regularly you reconcile, the sooner you catch issues like overcharges, missed payments, or fraudulent transactions.

- Accurate Cash Flow Management: With a real-time view of funds in and out, you can make better decisions about property improvements, staffing, and strategic growth.

- Reduced Stress at Period-End: Frequent checks mean fewer surprises during month-end or year-end closing, saving time and reducing the risk of large, retroactive adjustments.

- Enhanced Trust and Transparency: Timely, accurate books build confidence with investors, auditors, and stakeholders—demonstrating strong financial stewardship of vacation rental assets.

5. Overlooking Tax Deadlines and Regulations

Tax obligations for short-term rentals often vary by location, with numerous local and state regulations that may not apply to long-term rentals or other types of property management. Because of these variations, overlooking certain deadlines or failing to collect specific occupancy taxes is a common issue—and the repercussions can include fines, penalties, and strained relationships with local authorities.

Many property managers operate under the assumption that filing an annual return is sufficient, only to discover too late that monthly or quarterly taxes are required. This discrepancy may result in retroactive fees or legal complications, throwing a wrench into an otherwise well-managed operation. Teams may also miss opportunities for valid deductions if they are unaware of tax rules unique to short-term rentals.

The most effective strategy to avoid these pitfalls is to stay informed and organized. Maintaining a master calendar of filing deadlines for each jurisdiction where properties are located helps the team anticipate due dates and prepare documents in advance. For managers who operate across multiple locales, consulting with a tax professional or an accountant specializing in short-term rentals provides clarity on local regulations. There are a handful of property management software solutions that also offer integrated tax modules, calculating and sometimes remitting the appropriate occupancy taxes on the manager’s behalf. By taking a proactive approach to tax compliance, property managers safeguard their revenue and maintain a reputation for professionalism.

How to Create a Tax Compliance Calendar

- Identify Applicable Jurisdictions

- List out every city, county, or state where your properties are located.

- Research or consult with a professional to confirm the specific tax requirements (e.g., occupancy tax, tourism tax, sales tax).

- Determine Filing Frequency

- Check whether the taxes need to be filed monthly, quarterly, or annually.

- Note any additional due dates for payment versus filing (they don’t always coincide).

- Gather Key Deadlines and Information

- Record the exact due dates for each tax in each jurisdiction.

- Make note of what information or forms need to be submitted (e.g., specific occupancy reports, revenue statements).

- Use a Centralized System

- Maintain a single calendar—whether it’s a spreadsheet, a shared team calendar, or a specialized compliance tool—where all deadlines and reminders are stored.

- Assign responsibility: each filing requirement should be clearly owned by a member of the team or an external accountant.

- Set Reminders and Alerts

- Schedule automated reminders at least one week in advance of each filing deadline.

- If your property management system or accounting software supports custom notifications, enable them to stay on track.

- Review and Update Regularly

- Tax regulations can change. Review your calendar at least once a year—or more often if you operate in rapidly changing jurisdictions.

- Include any newly acquired properties or newly implemented tax requirements as soon as they arise.

- Track Payments and Confirm Receipts

- After submitting a filing and payment, record the confirmation number or receipt from the tax authority.

- Update the calendar to reflect that the task is completed, ensuring there’s a clear history of compliance.

Why a Proactive Tax Calendar Matters

- Avoid Fines and Penalties: Consistently meeting deadlines helps you sidestep late fees, which can snowball quickly if overlooked for multiple properties.

- Maintain Professionalism: Showing local authorities and partners that you handle taxes punctually boosts trust and credibility.

- Optimize Deductions: Having a clear timeline and organized documentation ensures that you capture all eligible deductions and credits.

- Simplify Year-End Tasks: Regular, scheduled tax compliance throughout the year reduces stress and complexity when preparing final returns or annual reports.

- Build Strong Relationships: Staying compliant fosters a positive rapport with local governments and communities, which can be especially important if you’re seeking permits or planning to expand.

By creating and diligently following a tax compliance calendar, short-term rental managers can reduce stress, minimize financial risks, and keep operations running smoothly—regardless of how many different tax regimes they need to navigate.

Preventing Future Mistakes and Staying Profitable

Across these five common accounting mistakes, a recurring theme emerges: the absence of clear, standardized financial processes. Whether it is keeping personal and business funds separate, implementing a robust record-keeping system, embracing accrual-based accounting, scheduling regular reconciliations, or remaining vigilant about local tax deadlines, the solution lies in disciplined procedures and the right technology tools.

Formalizing such practices not only reduces the margin for error but also empowers property managers to make timely, informed decisions about their portfolios. By documenting standard operating procedures for everything from expense approvals to revenue recognition, the entire team can maintain consistency and transparency. In addition, modern property management software that integrates bookings, expenses, and tax obligations streamlines the workload significantly, minimizing both manual entry and guesswork.

Jed Stevens, co-founder of Koloa Kai Vacation Rentals, emphasizes the value of standardized financial processes: 'With Topkey, I categorize the expense by property and which of the accounts in Quickbooks it belongs to. Then I hit 'sync', and it goes to Quickbooks, and I don't have to touch it again. It's a huge relief.' This automation saves his team at least eight hours every month while dramatically improving accuracy—time they now invest in enhancing guest experiences and growing their business."

FAQ:

What accounting software is recommended for vacation rental managers?

A: Most vacation rental managers use an accounting system like Quickbooks combined with Topkey for expense management and PMS integrations and receipt capture.

How often should I reconcile my accounts?

A: Monthly or weekly reconciliation is recommended for accuracy.

What are the tax implications of owning a vacation rental property?

A: Tax implications vary by location; consult a tax professional for specific guidance.

Is a separate business bank account necessary?

A: Yes, it is highly recommended to keep business and personal funds separate.

How can I track occupancy taxes?

A: Use property management software or maintain accurate records.

Conclusion

Although the vacation rental industry can present complex accounting challenges, most issues stem from a handful of recurring errors. By proactively addressing these five mistakes—mixing funds, failing to keep detailed records, inaccurately recognizing revenue, reconciling infrequently, and overlooking tax obligations—property management businesses can protect profits, reduce stress, and build a solid foundation for growth.

Establishing best practices for financial management not only improves daily operations but also enhances the overall guest experience, as managers can focus less on administrative tasks and more on hospitality. For those seeking additional guidance or customized solutions, a specialized property management accounting platform or consultation with an expert can provide the structure and clarity needed to stay ahead in an ever-evolving market. When records are accurate and compliance is maintained, property managers can confidently scale their operations, knowing their finances will remain stable and well-organized.

See the Topkey difference.